SWIFT vs Stablecoin Rails: A Modern Alternative to the SWIFT Payment System

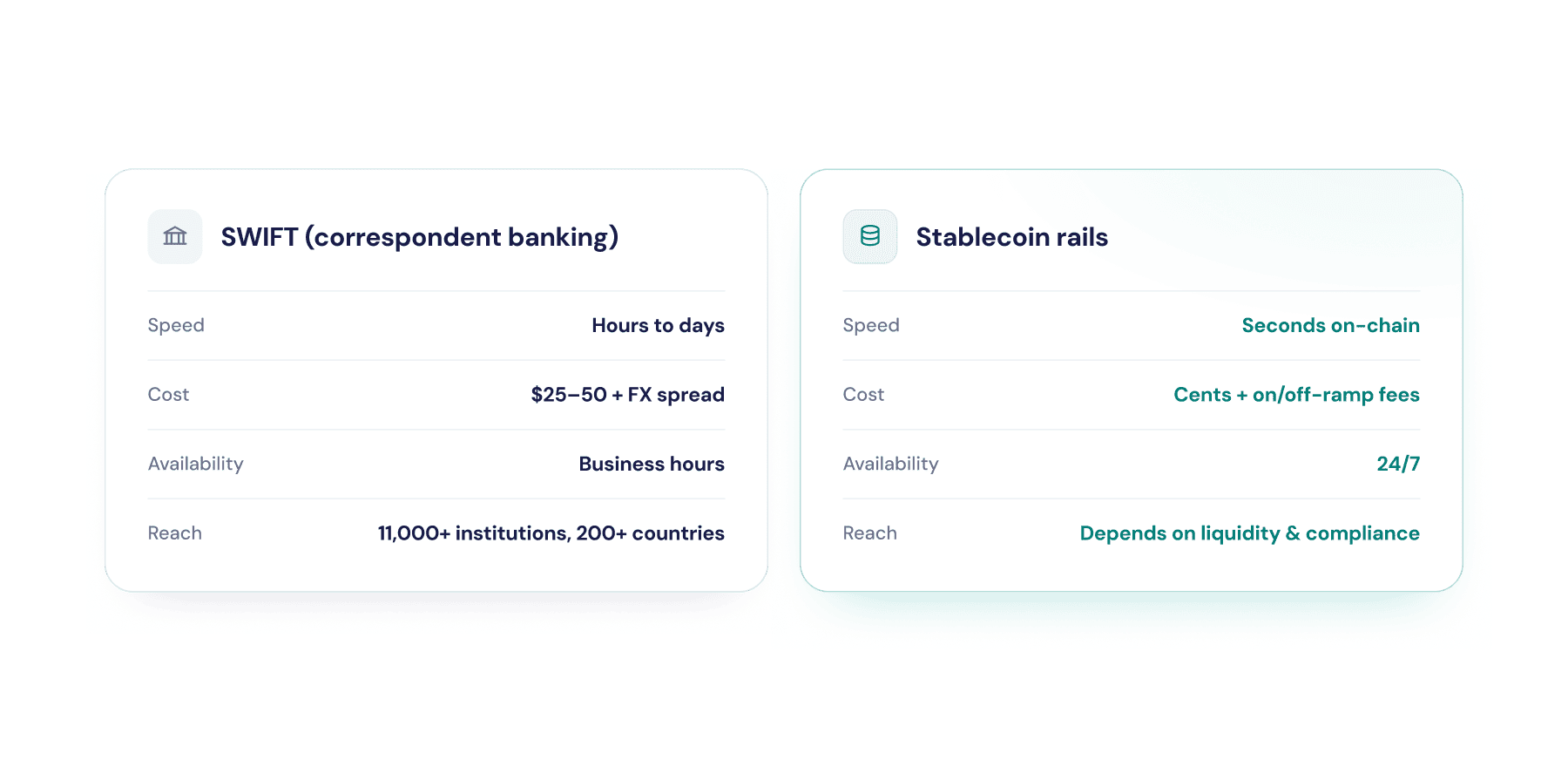

- SWIFT carries messages, not money. It tells banks how to move funds; settlement still flows through chains of correspondent banks. That chain makes cross‑border payments costlier and slower. Retail remittances still cost about $12 to send $200 and often take multiple days.

- Stablecoin rails move value directly. A sender converts local currency to a stablecoin, transfers it on‑chain, and the recipient converts back to fiat. This shortens the chain and can reduce delays and charges. These rails don’t replace SWIFT but offer an alternative for corridors where speed, transparency and cost matter most.

- Merge combines both worlds. Its platform pairs stablecoin rails with local payment networks, so firms collect in local currencies and settle across borders without managing correspondent relationships. Built‑in compliance and regulation by France’s AMF make it a regulated alternative.

Cross-border payments sit at the centre of global trade, yet many businesses still rely on infrastructure built around correspondent banking networks. The SWIFT payment system remains the standard for international bank-to-bank messaging, connecting thousands of financial institutions worldwide. Yet businesses often face extra costs, limited visibility and settlement delays once payments move through multiple intermediaries.

This guide compares the SWIFT system and stablecoin rails side by side. You'll learn how the SWIFT payments system works, where costs and delays originate, how stablecoin-based settlement differs, and why many companies now explore a SWIFT alternative for cross-border payments. We also examine speed, cost, compliance and real-world use cases, then show how Merge combines stablecoin rails with local payment networks to help businesses collect locally and pay out globally.

What Is SWIFT and How Does the SWIFT Payment System Work?

To compare SWIFT and stablecoin rails fairly, it helps to understand what SWIFT actually does and where payment settlement occurs.

SWIFT is Messaging, not Settlement

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) is a cooperative owned by financial institutions. It provides a standardised messaging network that banks use to instruct each other how to move funds and settle trades. SWIFT does not hold accounts or move money; it sends secure messages. Payments initiated through SWIFT GPI move quickly at the message layer, 60% of GPI transactions credit the beneficiary bank within 30 minutes, and nearly all within a day. The messaging network itself is fast and safe.

Where the Cost and Delay Actually Come From

When a business in Amsterdam pays a supplier abroad, the funds typically flow through a chain of banks. Each bank maintains nostro and vostro accounts in other jurisdictions and uses SWIFT to exchange messages. Every leg adds compliance checks, foreign‑exchange spreads and correspondent fees. The Bank for International Settlements notes that sending a $200 remittance still costs about $12, around 6%, and can take multiple days. A Harvard Business School study finds that cross‑border bank wires charge FX mark‑ups of 200-400 basis points even for liquid currency pairs.

The delay is not from SWIFT but from correspondent banking. Banks must reconcile ledgers across time zones, perform anti‑money‑laundering checks and manage liquidity.

What Are Stablecoin Rails?

A stablecoin rail is an infrastructure that uses a stablecoin, a digital token backed one‑to‑one by fiat currency, to move value across borders. The sender converts local currency into a stablecoin, transfers it via a public or permissioned blockchain, and the recipient or their bank converts it back into local fiat. Because the transfer occurs on‑chain, the settlement is near‑instant and operates 24/7.

Distributed-ledger technology can reduce complexity, costs and delays in cross‑border payments by enabling real‑time settlement and providing an immutable record. Payment‑stablecoin models shorten the chain by connecting smaller banks directly and can reduce end‑user costs by eliminating institutional overheads. Yet they do not remove all intermediation, users still need on‑ramps, off‑ramps and trusted exchanges.

SWIFT vs Stablecoin Rails: Side‑by‑Side Comparison

Speed and Settlement

SWIFT GPI has improved transparency and speed, yet the overall settlement time still depends on correspondent banks. Many banks can only credit customers during business hours, so part of a payment’s life is spent waiting. Stablecoin rails eliminate the need for several correspondent legs. A payment moves on‑chain within seconds and can be credited as soon as the receiving institution converts it to fiat. This is particularly useful for time‑sensitive treasury and payroll flows.

Cost and Transparency

Traditional rails bundle multiple cost components: wire fees, FX spread, correspondent bank deductions and opportunity costs from funds held in transit. Stablecoin transfers avoid correspondent deductions and can provide mid‑market FX rates, but users face exchange fees and on‑chain transaction costs. Net savings vary by corridor.

Coverage and Reach

SWIFT’s reach makes it indispensable. It links banks in almost every jurisdiction, supports many currencies and integrates with local clearing systems. Stablecoin rails are widely accessible on public blockchains, yet depend on the availability of liquid stablecoins for the currency pair in question. Juniper Research predicts cross-border B2B stablecoin transaction value will grow from $13.4 billion in 2026 to $5 trillion by 2035. This suggests increasing reach but is still far below SWIFT volumes.

Compliance and Controls

Regulators require banks to perform KYC, AML and sanctions checks. These obligations continue under stablecoin rails. The U.S. Federal Reserve observes that payment stablecoins could reduce end‑user costs by eliminating some institutional overheads, but banks may still mediate stablecoin flows to maintain inventories and conduct compliance. Merge builds compliance into its platform, offering transaction monitoring, PEP screening and sanctions checks as part of every transfer.

SWIFT vs Fedwire vs Stablecoin Rails

It can be tempting to compare SWIFT to Fedwire. Fedwire is the Federal Reserve’s domestic wire system that settles funds in U.S. dollars in real time between banks in the United States; it is not used for cross‑border transfers. SWIFT is a messaging service used globally to instruct payments, whereas stablecoin rails combine messaging and settlement on a blockchain. Stablecoin transfers can function like a cross‑border version of Fedwire, but their efficacy depends on liquidity and regulatory acceptance.

Why Do Businesses Look for an Alternative to the SWIFT Payment System

Businesses seek alternatives for several reasons. Cost stands out: correspondent banking fees, FX spreads, and wire charges add up, and the final amount received may be lower than expected. Timing is another factor. Even with SWIFT GPI improvements, funds may take hours or days to settle because of time zones and intermediary processes. For firms managing global supply chains or payroll, waiting days to receive funds can create working‑capital stress. Transparency is also limited; senders often lack visibility into deductions and processing times.

Failed payments further complicate matters. Merchants experience higher failure rates on cross‑border payments compared with domestic transactions. Each failure results in manual investigations and additional costs. Businesses with high transaction volumes are therefore exploring alternative rails that offer predictability, traceability and real‑time settlement.

Where Stablecoin Rails Fit and Where SWIFT Still Makes Sense

No payment rail is right for every use case. The choice depends on the corridor, settlement requirements, regulatory environment and the type of transaction being processed.

In practice, many businesses use both. SWIFT remains the backbone of international banking, with broad coverage and established compliance processes. Stablecoin rails can complement that infrastructure by providing an additional settlement option for specific corridors, treasury flows and time-sensitive payments. For many global businesses, a blended model delivers the flexibility of stablecoin settlement alongside the reach and familiarity of the SWIFT payment system.

How Merge Combines Stablecoin Rails with Local Fiat Networks

Merge connects to more than 100 local payment networks, including ACH in the U.S., SEPA in Europe, Faster Payments in the UK, PIX in Brazil and SPEI in Mexico and more. Clients can collect funds in local currency and have them converted into stablecoins for cross‑border settlement. Once settled on‑chain, Merge pays out on another local rail, so both the sender and recipient transact in their own fiat currency. Settlement occurs 24/7, without banking‑hour limitations, and automated reconciliation makes matching payments straightforward.

Instead of integrating with multiple banks and payment processors, businesses integrate once with Merge’s unified API. They can open sub‑accounts for different clients or transaction types, convert between fiat and stablecoins, and trigger payouts across borders. Transparent, flat‑fee pricing means costs are predictable, and dedicated sub‑accounts with auto‑matching reconciliation simplify accounting.

A Practical Alternative to the SWIFT Payment System

SWIFT remains the backbone of international banking. It delivers reliable messaging and, with gpi, faster and more transparent payments. Yet for many businesses, the correspondent banking chain still brings high costs and delays. Stablecoin rails offer a modern alternative by moving value directly on‑chain and connecting local payment networks worldwide. They do not replace SWIFT; they complement it in corridors where speed, transparency and cost are paramount.

Merge combines these worlds. Its regulated platform links stablecoin settlement with over a hundred local fiat networks, handles compliance in the background and offers a single API for global payouts. To learn more about how stablecoin rails can supplement your cross‑border strategy, talk to Merge and explore their API.

FAQ

What is the SWIFT payment system?

SWIFT is a global messaging network that lets banks securely send standardised payment instructions to one another. It doesn’t hold or move funds itself; settlement still happens through chains of correspondent banks. That separation between messaging and settlement is why cross‑border bank payments can involve several intermediaries and delays.

What are stablecoin rails?

Stablecoin rails use digital tokens pegged to fiat currency to move value directly between parties. In Merge’s model, funds are collected on a local payment rail, settled via stablecoins and paid out on another local rail. Transfers happen on‑chain, so cross‑border payments remain in fiat at both ends and settle quickly.

SWIFT vs stablecoin rails: which is faster and cheaper?

It depends on the corridor and flow. SWIFT messages travel instantly, but settlement depends on correspondent banks and can take hours or days. Stablecoin rails can shorten settlement to seconds and reduce bank fees, though on‑ramp/off‑ramp costs and exchange spreads still apply. The right choice depends on your corridor, currency pair and compliance requirements.

Is there an alternative to the SWIFT payment system?

Yes, for many cross‑border flows, stablecoin‑based infrastructure offers an alternative. Juniper Research forecasts that cross‑border B2B stablecoin transactions will grow from $13.4 billion in 2026 to $5 trillion by 2035. Merge combines stablecoin rails with 100+ local payment networks and built‑in compliance, allowing businesses to collect locally and pay globally without managing multiple correspondent relationships.

Are stablecoin rails regulated and safe to use?

Regulation varies by jurisdiction. Payment stablecoins are subject to rules that require issuers to back tokens with safe assets and comply with KYC/AML standards. Merge is a regulated payment and e-money institution in France and embeds compliance checks into every transaction. Firms should always verify the licensing and security standards of their provider.

Disclaimer: This content is intended for informational purposes only. It should not be considered financial, legal, or operational advice. Businesses should evaluate their own compliance, regulatory, and infrastructure requirements before implementing payment solutions.