What Is a Multi‑Currency Account? Enterprise Guide

- One account, many currencies: A multi-currency account gives a business a single place to receive, hold, and send funds in more than one currency. Rather than juggling a EUR account, a GBP account, and a USD account, you can maintain balances across currencies within one structure, reducing conversion fees and administrative overhead.

- Operational efficiency at scale: Enterprises use multi-currency accounts to reduce the complexity of cross-border collections, payables, and reconciliation. Local bank details, transparent FX, and sub-accounts enable finance teams to manage global cash flows with greater visibility, control over timing, and automation.

- Modern infrastructure overcomes legacy limitations: Traditional currency accounts or SWIFT-based systems are constrained by slow transfers and fragmented workflows. Modern multi-currency business accounts, especially those built on stablecoin rails like Merge, support 60+ currencies, real-time transfers, and API-driven integrations for treasury, marketplaces, and platforms.

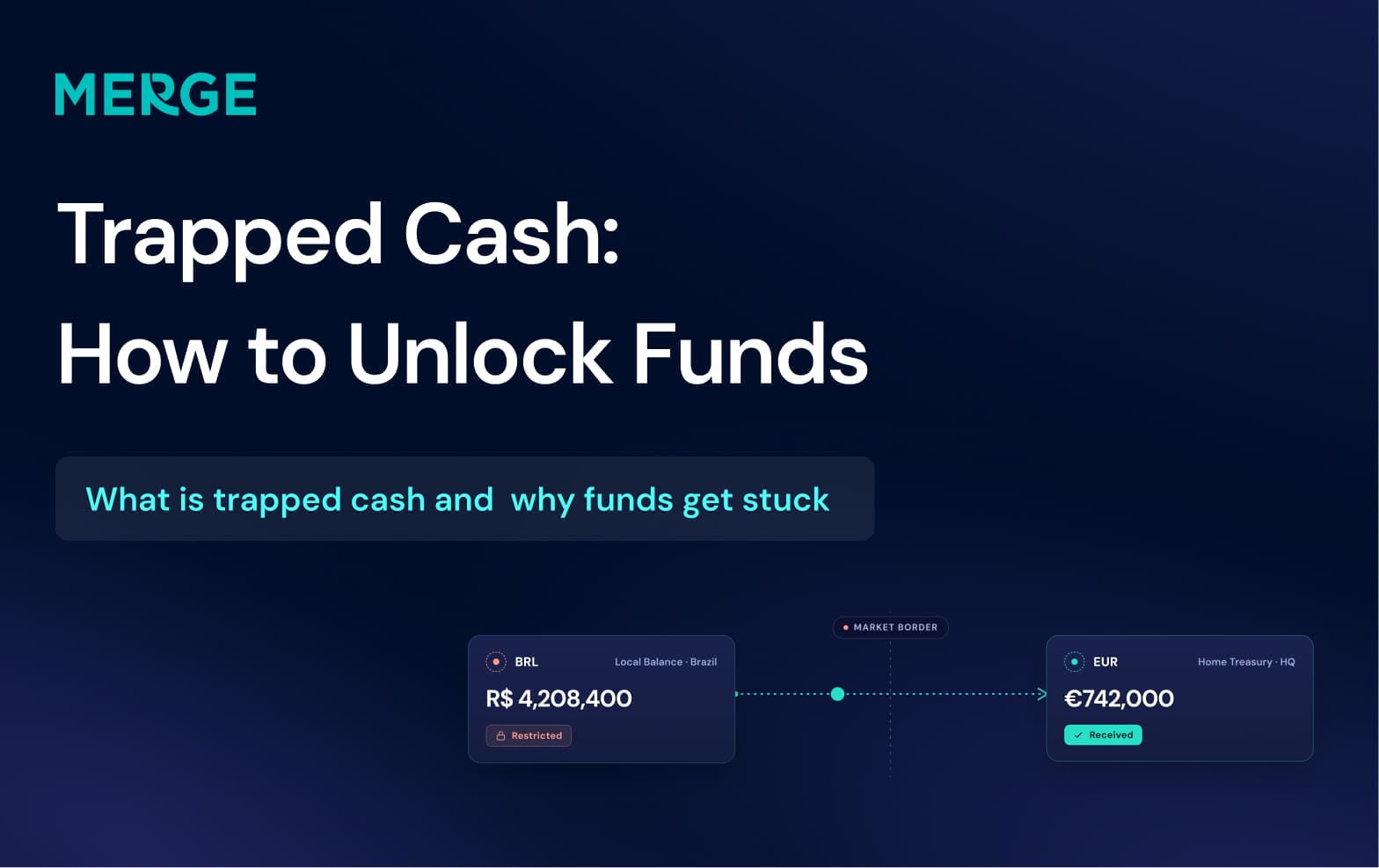

Cross‑border commerce has become the norm rather than the exception. Finance teams still rely on fragmented banking setups to manage international flows. Multiple accounts, forced currency conversions and opaque FX costs create friction at every stage. What should be routine, collecting revenue, paying suppliers, and reconciling transactions, becomes unnecessarily complex.

Consider a UK-based SaaS company scaling across markets. It invoices customers in dollars, pays contractors in euros and settles marketing spend in Singapore dollars. Under a traditional model, this means maintaining separate accounts, navigating intermediary banks and absorbing avoidable conversion costs. The process slows down cash flow and introduces operational risk.

A multi-currency account changes that structure entirely. It allows businesses to receive, hold and move funds across currencies within a single account, removing the need for fragmented banking relationships and giving finance teams direct control over FX and liquidity.

In this guide, we break down what a multi-currency account is, how it works in practice, how it compares to a multi-currency bank account, and why it has become a core component of enterprise payment infrastructure.

What this looks like with Merge:

What Is a Multi-Currency Account?

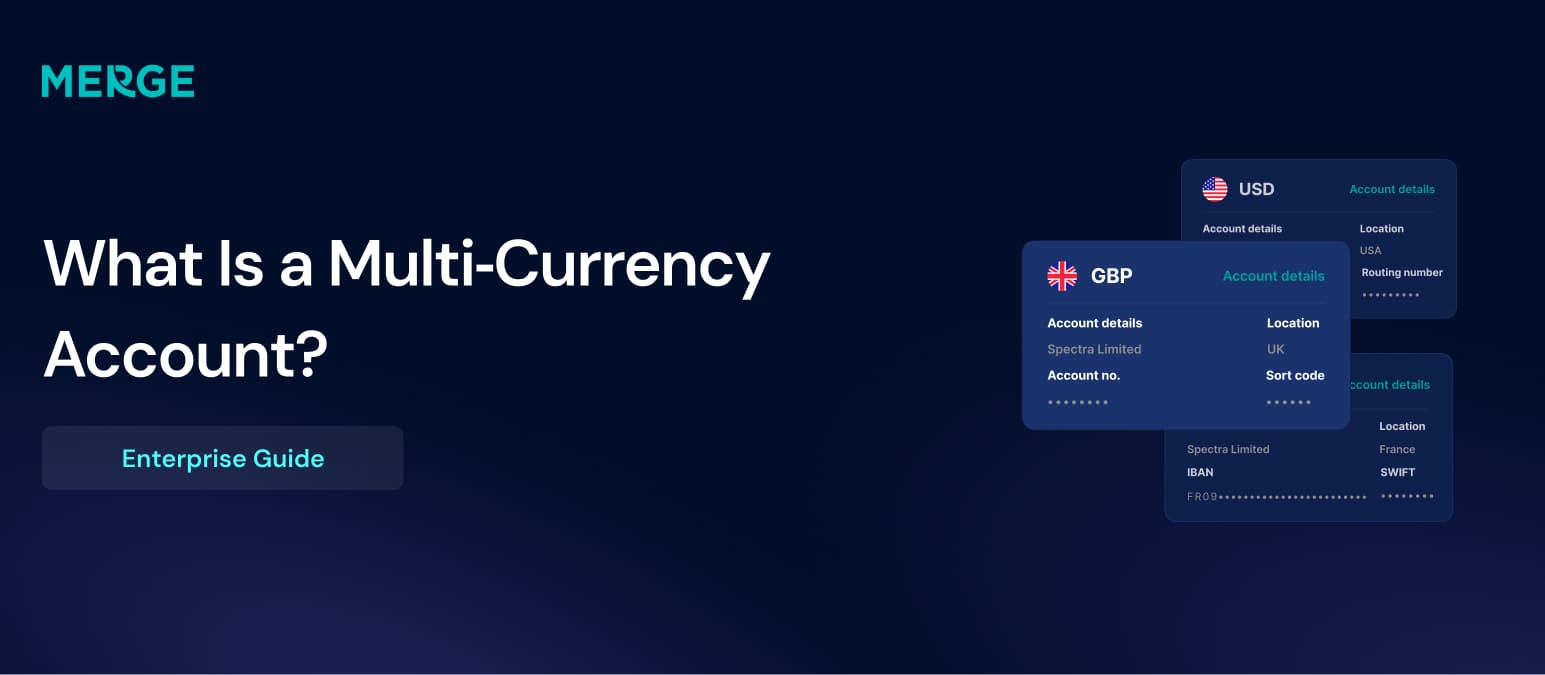

A multi-currency account is a financial account that supports multiple currencies at once. Instead of opening a separate bank account for each currency, you open a single account that lets you hold, receive, convert and send funds in different currencies. Providers deliver local bank details (such as IBANs or routing numbers) for several countries, so your international clients can pay you via their domestic rails. The account consolidates balances in currencies such as USD, GBP, EUR and others into one dashboard, giving enterprises a unified view of their global cash position.

This structure differs from a currency account, which typically allows you to hold a single foreign currency. Currency accounts are useful for occasional transactions, but become unwieldy as you expand into new markets. A multiple-currency account or multi‑currency bank account solves that by letting you manage many currencies within one account. Modern fintech providers even extend the concept into stablecoin wallets.

The distinction between “multi-currency account” and “multi-currency bank account” is largely terminological. Traditional banks may refer to their offering as a “multicurrency bank account” or “multiple currency account” to emphasise the banking licence, whereas fintech platforms use a multi-currency account or multi-currency business account to highlight digital features such as API access and sub‑accounts.

How Does a Multi-Currency Account Work?

At a high level, a multi-currency account brings together the functions of receiving, holding, converting and reconciling funds across currencies:

- Receiving: The provider issues local banking details in multiple countries. When a client pays you in euros or pounds, the money arrives via domestic payment networks such as SEPA or Faster Payments, avoiding SWIFT fees. Modern platforms like Merge also issue stablecoin deposit addresses, enabling businesses to on‑ramp fiat into digital tokens and receive funds from blockchain networks.

- Holding: Balances in each currency sit within one interface. You might see £50,000, €30,000 and $100,000 side by side and decide whether to convert or hold.

- Converting: You can convert between currencies at interbank or market rates. Some providers allow you to time conversions based on cash‑flow needs. With a multi-currency account, you can hedge future payments with forward contracts or lock in rates.

- Reconciliation: Multi-currency accounts integrate reconciliation features so that incoming and outgoing payments are matched automatically. Merge’s intelligent reconciliation engine uses sub‑accounts and webhooks to assign payments to orders, reduce manual effort and provide real‑time reporting.

Behind the scenes, these accounts rely on a mix of traditional bank partnerships, local payment schemes and, increasingly, stablecoin rails. Payments on stablecoin networks settle within minutes rather than days, and on/off‑ramp services convert fiat to stablecoin and vice versa while segregating funds in regulated accounts. This combination is what allows modern multi-currency accounts to operate across 75+ countries and 60+ currencies while offering near‑instant settlement.

Multi-Currency Account vs Multi-Currency Bank Account

The terms multi-currency account and multi-currency bank account are often used interchangeably, but there are practical differences:

- Traditional multi-currency bank account: Offered by banks, this account is typically anchored to a primary currency with additional currency “pots.” You may be required to open the account in a specific country or maintain a minimum balance. Transfers usually rely on SWIFT, which introduces intermediary banks, higher fees and slower settlement times.

- Modern multi-currency account: Built by fintech providers and platforms, this account operates digitally and supports a broad range of currencies, often 40–60+. It provides local bank details in several jurisdictions and offers real‑time conversion and payments. These accounts often include sub‑accounts, API access and automated reconciliation features.

- Multiple currency accounts and IBAN differences: A multi-currency IBAN allows you to receive payments in dozens of currencies under a single International Bank Account Number. B2B Pay notes that with traditional accounts, you either receive one currency or the bank converts incoming funds immediately. Multi-currency accounts, by contrast, let you hold funds in each currency until you choose to convert.

Enterprises should therefore consider whether a multi-currency bank account from a legacy provider meets their needs or whether a multi-currency business account delivered by a fintech provides the flexibility, speed and automation required for today’s cross‑border operations.

Why Enterprises Use Multi-Currency Accounts

- Reduce operational complexity: Managing separate bank accounts for each currency is administratively heavy. Teams must track balances across systems, update account details for every supplier and deal with inconsistent cut‑off times. A multi-currency account consolidates currencies into one interface and reduces duplication. Businesses save hours of reconciliation and avoid double conversions by using a multi-currency account.

- Improve visibility across currencies: Visibility over global cash positions is critical for treasury teams. With a multi-currency account, finance leaders see balances across currencies in real time and can decide when to convert or hold. The ability to pre‑fund balances and choose when to convert protects margins and gives timing certainty. The consolidated view also simplifies reporting and helps controllers forecast cash flow more accurately.

- Support cross‑border collections and payouts: Enterprises selling across borders need to accept payments from customers in their local currencies and pay suppliers or contractors globally. Multi-currency accounts enable local collection via domestic rails and real‑time payouts. Merge’s platform supports payments in 60+ currencies and issues IBANs to sellers, enabling marketplaces to collect and disburse funds in the currencies of their choice.

- Simplify treasury and reconciliation: Automated reconciliation is a critical feature for enterprise finance teams. Merge’s intelligent reconciliation module assigns dedicated sub‑accounts to customers or lines of business, matches incoming and outgoing payments and provides real‑time reporting. This reduces manual effort and minimises errors. In addition, being able to schedule conversions and hedge FX exposures helps treasury teams manage currency risk.

Avoid unnecessary banking fragmentation: Without multi-currency accounts, businesses often open several bank accounts across jurisdictions, leading to trapped cash and expensive transfers. Multi-currency business accounts centralise funds and allow them to move freely between currencies and networks. With stablecoin rails, funds settle almost instantly and can be off‑ramped into local accounts. This unified infrastructure reduces the need for multiple banking relationships and minimises trapped liquidity.

Named IBANS: A Step Beyond Virtual Accounts

As multi-currency infrastructure matures, one capability is emerging as a meaningful differentiator for enterprises operating at scale: named IBANs. Merge's Named EUR IBANs represent a major enhancement to its API-first payments infrastructure, enabling businesses to issue fully named, dedicated EUR IBAN accounts to their end users and unlocking seamless fiat collection, reconciliation and payout capabilities across Europe.

Most virtual IBAN setups assign a routing reference to an end user, but the underlying account remains in the platform's name. This creates friction for reconciliation, for compliance, and increasingly for end users who expect to see their own name on the account they use to send and receive funds.

- Merge's Named EUR IBANs solve this directly. Rather than issuing a virtual reference layer, Merge opens fully functional EUR accounts in the name of the end customer. These accounts can receive, hold and send funds in their own right, and support both first-party and third-party payments, making them suitable for marketplaces disbursing to sellers, fintech platforms managing client funds, and regulated crypto-native companies bridging fiat and stablecoin rails.

- The practical implications are significant. For finance teams, named IBANs simplify reconciliation because each incoming payment is attributed to a specific, identified account from the outset.

For compliance teams, the named structure provides an auditable chain of ownership that satisfies KYC and AML requirements. And by combining dedicated IBAN accounts with its stablecoin payment capabilities, Merge enables clients to orchestrate end-to-end flows between fiat and digital assets, addressing a critical bottleneck that has long limited scalable, compliant cross-border infrastructure.

Key Features to Look for in a Multi-Currency Business Account

Not all multi-currency accounts are created equal. When evaluating providers, enterprises should consider the following features:

- Number of supported currencies: Check whether the provider offers the currencies relevant to your operations.

- Local bank details and real‑time rails: The ability to receive payments via local schemes (ACH, SEPA, Faster Payments, UPI, etc.) reduces fees and improves settlement times.

- Transparent FX and conversion tools: Compare FX spreads and consider whether the platform allows you to convert when rates are favourable. Multi-currency accounts let you convert at real‑time interbank rates and hold funds until you choose to exchange. Some providers offer forward or rate‑locking tools for hedging.

- Sub‑accounts and dedicated IBANs: Enterprises often need to segregate funds by client, region or product. Dedicated sub‑accounts and IBANs to segregate balances and automatically match payments. This is essential for regulated industries, marketplaces and investment platforms.

- API access and integration: A multi-currency business account should integrate into your payment flow and accounting software. API‑based payment initiation, balance retrieval and webhook notifications, enabling enterprises to automate FX, funding and reconciliation.

- Compliance and regulation: Cross‑border payments involve KYC, AML and reporting requirements. Look for a provider that handles compliance on your behalf. Infrastructure manages user onboarding, regulatory reporting and fraud protection, so businesses can focus on operations. Audit trails and SOC‑compliant security measures are also important for regulated industries.

Multi-Currency Accounts for Enterprise Payment Operations

Multi-currency accounts underpin many enterprise payment use cases:

- Vendor payments and procurement: Instead of converting funds for each invoice, a finance team can pay suppliers in their local currency from a dedicated balance.

- Payroll and contractor payouts: Paying a global workforce in their local currencies avoids hidden conversion costs for employees and ensures timely payments. Multi-currency business accounts support batch payments and maker‑checker approvals, making them suitable for payroll runs.

- Marketplaces and platforms: Marketplaces need to collect payments from buyers and disburse funds to sellers. Merge’s multi-currency accounts enable marketplaces to accept payments in 60+ currencies and segregate commission through sub‑accounts. Instant payouts improve liquidity for sellers and reduce chargebacks.

- Corporate treasury: Large enterprises manage cash positions globally and need to optimise working capital. Multi-currency accounts allow treasurers to hold funds in different currencies, convert when rates are favourable and move money across subsidiaries quickly. They reduce trapped cash and provide real‑time visibility into global liquidity.

- Embedded finance: Fintech platforms can embed multi-currency accounts into their products, enabling end users to hold and exchange currencies without leaving the platform.

When a Foreign Currency Account UK or Multi Currency Account UK Is not Enough

Some banks in the United Kingdom offer foreign currency accounts or multi-currency accounts for UK products. These accounts allow businesses to hold one or two foreign currencies, such as euros or dollars, and may be marketed as “euro account in UK” or “euro bank account in UK.” They are useful for receiving payments in a single foreign currency, but they often rely on SWIFT for cross‑border transfers, incur higher fees and provide limited currencies. For enterprises scaling into multiple markets, a foreign currency account in the UK is not sufficient. A multi-currency bank account in the UK from a legacy bank may support several currencies but lacks API integration and automated reconciliation.

Enterprises operating across Europe, Asia and the Americas benefit from a unified global money account, the modern multi-currency business account, rather than a patchwork of country‑specific accounts. By consolidating currencies, you eliminate the need for separate euro accounts in the UK, reduce FX overheads and simplify internal processes. When evaluating providers, ensure that “international transfer services” and “money transfer” capabilities cover both domestic rails and cross‑border payment processing, including local payouts in 60+ countries.

How Merge Supports Enterprise Multi-Currency Accounts

Merge is a regulated payments and treasury infrastructure platform backed by Coinbase and Octopus Ventures. It integrates stablecoin rails, local bank networks and FX to provide a comprehensive multi-currency business account. Key aspects include:

- 60+ currencies and 75+ countries: Merge’s multi-currency account lets businesses receive, hold and exchange over sixty currencies across more than 75 countries.

- Sub‑accounts and real‑time rails: Dedicated sub‑accounts and IBANs allow you to segregate customer funds and reconcile them instantly. Real‑time payment rails enable instant transfers between fiat and stablecoin balances via on/off‑ramp infrastructure.

- API‑first design: Merge’s API allows enterprises to create accounts, issue payment instructions, subscribe to webhooks for payment updates and automate treasury flows. Global real‑time payments and intelligent reconciliation modules provide payment initiation, event notifications and compliance management.

- Stablecoin orchestration: By bridging fiat and stablecoin networks, Merge helps businesses move money across borders faster and more cost‑effectively than SWIFT. Funds are held in regulated accounts and can be off‑ramped into local bank accounts or on‑ramped into USDC or EURC. This architecture reduces settlement times from days to minutes and minimises FX spreads.

- Compliance and security: Merge handles KYC, KYB, AML and regulatory reporting on behalf of customers, providing multi‑factor authentication and SOC‑compliant security measures. This is essential for enterprises operating in regulated sectors.

- Integrations with other products: Through its platform, Merge links multi-currency accounts with its Stablecoin On/Off Ramp, Global Real Time Payments and Intelligent Reconciliation modules. Finance leaders can build end‑to‑end payment flows across currencies, from collecting funds to reconciling invoices and sweeping balances into corporate treasury. The platform’s infrastructure layer thus unifies global payments, FX and liquidity management.

Book a personalised demo to see how Merge simplifies multi-currency accounts, global payments, and reconciliation across your business operations.

FAQ

What is a multi-currency account?

A multi-currency account is a single financial account that allows you to receive, hold, convert and send funds in multiple currencies. It provides local bank details for different markets and consolidates balances in one place, giving businesses greater control over FX and global cash flows.

How does a multicurrency bank account work?

A multi-currency bank account works by allocating separate “pots” for each currency under one account number. Payments received in each currency are credited to the relevant pot, and you can transfer funds between pots at bank‑determined rates. Modern providers offer real‑time conversion, local rails and API access to automate these processes.

What is the difference between a multi-currency account and a currency account?

A currency account usually lets you hold a single foreign currency. A multi-currency account, by contrast, enables you to hold multiple currencies simultaneously, reducing the need for separate accounts and enabling consolidated reporting.

Why do enterprises use multi-currency accounts?

Enterprises use multi-currency accounts to reduce operational complexity, improve visibility across currencies, support global collections and payouts, simplify treasury and reconciliation and avoid unnecessary banking fragmentation. These accounts also give businesses more flexibility over when to convert and help them manage FX risk.

Is a multi-currency business account the same as a foreign currency account in the UK?

No. A foreign currency account UK typically holds a single currency, such as euros or dollars, for a British business. A multi-currency business account supports numerous currencies and provides features like API access and automated reconciliation. Enterprises operating across several markets should look beyond single‑currency accounts.

Disclaimer: This content is intended for informational purposes only. It should not be considered financial, legal, or operational advice. Businesses should evaluate their own compliance, regulatory, and infrastructure requirements before implementing payment solutions.