Payment Orchestration vs Payment Gateway: What's the Difference?

- Payment gateways handle the front‑end act of authorising and transmitting payments. They sit between a checkout and an acquirer, collecting payment data and forwarding it for approval.

- Payment orchestration platforms manage the whole payment operation. They centralise gateways, processors and acquirers, route transactions intelligently and handle reconciliation, reporting and optimisation. They’re designed for businesses operating across markets, payment methods and currencies.

- For small, single‑market merchants, a simple payment gateway may suffice. Businesses scaling across borders or juggling multiple providers need the flexibility, redundancy and data visibility that orchestration brings.

As businesses expand, their payment infrastructure often evolves from a basic gateway into a more sophisticated operation. A payment gateway authorises payments and passes transaction data securely between customers, merchants and banks. Payment orchestration, by contrast, is a control layer that unites multiple gateways and payment service providers under one API, enabling smarter routing, failover and reconciliation. Understanding the differences between these two models is essential for operators, fintech founders and treasury teams who must decide which model suits their needs today and tomorrow.

Payment gateways help businesses accept payments, while payment orchestration helps them run a payment operation. A gateway collects and encrypts payment details, then transmits them to an acquirer for authorisation. An orchestration platform centralises those gateways and providers, manages routing and retries, and produces unified reporting across markets. Businesses often start with a gateway, then adopt orchestration as their operations become more complex.

Payment Orchestration vs Payment Gateway at a Glance

Note: Some payment service providers (PSPs) bundle gateway, acquiring, and basic routing functions in a single product. As transaction volumes and market complexity grow, dedicated orchestration platforms offer routing flexibility, provider redundancy, and analytics that bundled PSPs don't match.

What Is a Payment Gateway?

A payment gateway is the technology that enables businesses to accept electronic payments both online and in person. It acts as a bridge between a merchant’s website or point-of-sale system and the financial institutions that process transactions. Many modern payment gateway solutions handle this process by securely collecting, encrypting and transmitting customer payment data to the acquiring bank for verification. Once the issuing bank approves or declines the transaction, the gateway sends a confirmation back to the merchant, concluding the sale.

For businesses operating in specific regions, such as the United Kingdom, choosing the right UK payment gateway can also influence authorisation rates, supported payment methods and settlement efficiency.

How Gateways Work

- Data collection and encryption – At checkout, the gateway collects card or alternative payment details and applies encryption or tokenisation to protect sensitive data.

- Authorisation request – The gateway forwards the encrypted data to the payment processor or acquiring bank to request authorisation. This involves contacting card networks and the issuing bank to check the shopper’s funds or credit limit.

- Response and confirmation – The issuing bank sends an approval or decline message back through the network. The gateway relays this response to the merchant, allowing them to complete or reject the order.

Because gateways focus on authorising transactions, they are best suited to merchants with low to moderate transaction volumes and simple payment flows. They support a limited set of payment methods and currencies; adding new methods often requires integrating additional gateways or processors.

What Is Payment Orchestration?

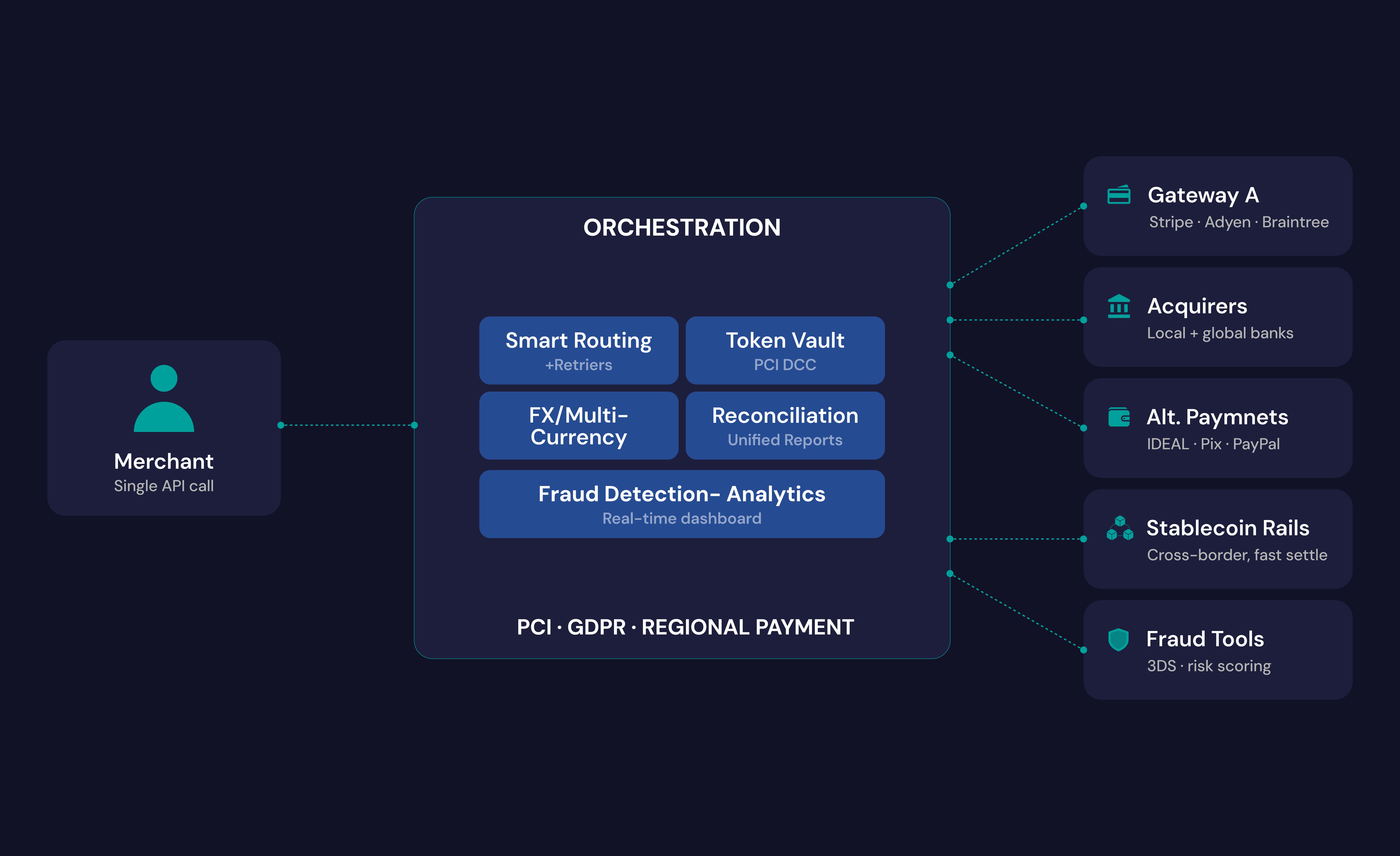

Payment orchestration is the process of centralising payment gateways, processors, acquirers and other financial service providers through a single platform. Rather than integrating and maintaining each provider separately, a business connects to an orchestration platform once and manages its entire payment stack from there. The platform then handles transaction routing, retries, tokenisation, fraud detection, multi-currency flows and reporting across all providers.

This model has become increasingly important for companies operating internationally, where global payment orchestration allows businesses to manage payments across multiple markets, currencies and local payment rails through one unified infrastructure. As a result, many fast-growing companies now evaluate the best payment orchestration platforms to improve approval rates, simplify integrations and gain greater control over their payment operations.

How Orchestration Works

- Unified integration – Payment orchestration platforms aggregate gateways, payment service providers (PSPs), acquirers and alternative payment methods into a single API. This eliminates the need for multiple integrations and reduces complexity when adding new providers.

- Smart routing and retries – When a customer initiates a transaction, the orchestration engine evaluates criteria such as cost, success rates, currency, geography and regulatory requirements. It then routes the payment through the most appropriate provider and automatically retries failed transactions using alternate routes.

- Reconciliation and reporting – The platform reconciles settlement data from all connected providers into unified reports, providing real‑time visibility across the payment stack. This data feeds into analytics dashboards for monitoring authorisation rates, costs and customer behaviour.

- Security and compliance – Orchestration platforms often include token vaults, fraud detection and regulatory compliance tools. They help businesses reduce their PCI DSS scope by centralising sensitive data and applying advanced security measures.

Benefits of Orchestration

- Increased success rates – Access to multiple providers allows merchants to route transactions through the channel with the highest approval rates. Merchants using multi-gateway strategies typically report authorisation rate improvements of 2–10 percentage points, with higher gains in high-volume verticals such as travel and subscriptions.

- Lower costs – The platform optimises each payment for cost by selecting the provider with the most favourable fees and routing transactions through local rails. This reduces processing fees and foreign‑exchange spreads.

- Operational efficiency – Automating reconciliation, reporting and provider management frees finance and engineering teams to focus on growth. Unified dashboards provide a single source of truth for payment data.

- Global reach – Orchestration platforms support local payment methods, alternative payment methods and multiple currencies through one integration. They facilitate cross‑border payments and multi‑currency settlements by routing transactions to the best provider for each region.

- Resilience and redundancy – Built‑in failover ensures that if one provider goes down, transactions are automatically routed to another, maintaining uptime.

Key Differences Between Payment Orchestration and Payment Gateways

In practice, the difference between a payment orchestration platform and a payment gateway becomes clear when you look at how each handles providers, routing, reporting and global scale.

Scope

A gateway is focused on authorising individual transactions. It relays payment data between a merchant and a single acquiring bank. Payment orchestration platforms encompass one or more gateways and broaden the remit to include routing, retries, tokenisation, alternative payment methods and reconciliation.

Provider Management

Gateways require separate integrations for each acquirer or PSP. Merchants who operate in multiple markets may need to integrate and manage several gateways. In contrast, an orchestration platform offers a single integration that connects to numerous gateways, PSPs, fraud tools and alternative payment methods.

Smart Routing and Retries

A gateway typically routes payments through a single path, offering limited fallback options. Orchestration engines evaluate transaction data and send payments through the provider most likely to approve the transaction, then retry with alternate providers when necessary.

Reconciliation and Reporting

With gateways, each provider produces its own reports, forcing merchants to consolidate data manually. Orchestration platforms normalise settlement data across providers, offering unified reporting and analytics.

Geographic and Currency Flexibility

Payment gateways may support only a limited set of currencies and payment methods. Scaling into new regions often requires integrating additional gateways. Orchestration platforms support local and alternative payment methods across regions, allow transactions in multiple currencies and handle foreign‑exchange conversions.

Scalability for Enterprise Payments

Gateways can serve small merchants effectively, but they become cumbersome for high‑volume businesses. Adding new regions or payment methods means additional integrations and increased maintenance. Payment orchestration platforms are built for scale: they enable rapid onboarding of new providers, flexible payment routing and unified data management without re‑engineering.

When Is a Payment Gateway Enough?

For small merchants operating in a single market with straightforward payment flows, a simple payment gateway may cover all needs. If you accept only a handful of payment methods and route all transactions through one acquirer, the overhead of an orchestration platform may not be justified. In these cases, choosing the best payment gateway for your region and customer base can be enough to support reliable payment acceptance. However, businesses that later expand across borders may eventually need to integrate international payment gateways to support local payment methods and currencies in different markets. Reasons to stick with a gateway include:

- Single‑market focus – Your customers are in one country, and you only need local card acceptance.

- Limited payment methods – You accept credit and debit cards, plus perhaps one e‑wallet; no immediate plans to add alternative payment methods.

- Low transaction volume – Your volume is modest, and downtime risk from a single provider is acceptable.

- Simplified compliance – You’re comfortable managing PCI compliance directly and do not need advanced reconciliation or reporting.

Minimal engineering resources – You prefer to avoid the complexity of managing multiple providers or building custom routing logic.

When Payment Orchestration Becomes the Better Choice

Businesses often outgrow a single gateway as they expand across markets, currencies and payment methods. At that stage, adopting a payments orchestration platform becomes the obvious next step, giving businesses the infrastructure needed to manage multiple providers, payment methods and currencies through a single integration. Payment orchestration becomes the obvious choice when you:

- Operate in multiple markets – Cross‑border commerce introduces regional payment preferences, regulatory requirements and currency conversions. Orchestration platforms connect to local gateways and PSPs, letting you accept alternative payment methods like iDEAL in the Netherlands or Pix in Brazil without additional integrations.

- Run a marketplace or platform – Marketplaces need to collect payments from buyers and pay sellers. They must segregate commission, manage payouts and reconcile funds. A single gateway cannot handle the complexity; orchestration coordinates multi‑party flows across providers.

- Are you a fintech or treasury‑heavy operation? Fintechs often embed financial services, require real‑time balance management and need redundancy across providers. Payment orchestration supports intelligent routing, vaulting and reconciliation that allows them to focus on building the product rather than payments plumbing.

- Need multi‑currency and cross‑border settlement – Orchestration platforms manage currency conversions and route payments through local rails or stablecoin rails to minimise FX costs and settlement times.

- Seek redundancy and higher authorisation rates – Multi‑provider routing helps you maintain uptime, reduce declines and boost authorisation rates.

Want unified data and analytics – Consolidated reporting across providers allows you to analyse transaction trends, measure success rates and optimise your payment strategy.

Why the Distinction Matters for Global Payments

Global businesses face challenges that go beyond simply accepting payments. They must navigate local payment rails, multiple currencies, regulatory compliance, fragmentation among providers, and the burden of reconciliation. A payment gateway solves the problem of accepting a card payment; it does not solve the operational challenges of running a payment operation across borders.

Payment orchestration platforms help by:

- Supporting local rails and alternative payment methods – They connect to bank transfer schemes, e‑wallets and instant payment networks in dozens of countries, giving customers the payment options they expect.

- Managing multi‑currency flows – They route payments through providers that offer favourable FX rates and can settle in different currencies. They can also integrate stablecoin rails to bypass legacy correspondent banking systems, moving funds quickly across borders.

- Reducing provider fragmentation – By centralising connections to gateways, acquirers, fraud tools and PSPs, orchestration platforms reduce integration overhead and vendor lock‑in. They allow businesses to swap providers without major code changes.

- Automating reconciliation – They provide a single, normalised view of all transactions, settlements and payouts, reducing manual reconciliation work and improving cash visibility.

Complying with regional regulations – They incorporate built‑in tools for PCI DSS, GDPR and regional payment regulations.

How to Choose Between a Payment Gateway and a Payment Orchestration Platform

When deciding between a gateway and orchestration, evaluate your current operations and growth plans. Consider the following factors:

- Market footprint – Are you operating in one country or several? Will you expand to additional markets in the next year?

- Transaction volume – High volumes benefit from multi‑provider redundancy and optimisation, while low volumes might not warrant the extra complexity.

- Currencies and payment methods – Do you need to accept multiple currencies or alternative payment methods? Orchestration platforms support a wide array of payment options.

- Provider count – If you already work with multiple gateways or processors, consolidation under one orchestration platform can simplify management.

- Backup routing – Is downtime from a single provider an acceptable risk? Orchestration offers failover to minimise disruptions.

- Reconciliation burden – How much time do you spend reconciling settlements? Unified reporting can yield significant operational savings.

- Expansion plans – Do you intend to launch new products, support marketplaces or integrate with alternative rails? Orchestration provides the flexibility to adapt without major engineering work.

- Internal resources – Do you have the engineering capacity to manage multiple integrations, or would you rather offload complexity to a platform?

For many businesses, the answer isn’t “gateway or orchestration” but “both.” A gateway remains essential for authorising transactions; orchestration builds on that foundation to manage multiple gateways, optimise payments, and provide operational agility.

How Merge Supports Modern Payment Orchestration Needs

As an example of how modern orchestration platforms are evolving, here's how Merge, the company behind this article, approaches these challenges:

Stablecoin‑Powered Rails

Traditional cross‑border payments rely on networks of correspondent banks, which introduce delays, costs and trapped cash. Merge utilises stablecoin rails to send funds from a sender’s bank account through an on‑ramp to stablecoins, across a blockchain network and off‑ramp to fiat at the destination. This five‑step process can complete transfers in seconds rather than days and avoids correspondent banking fees.

Multi‑Currency Accounts and Global Coverage

Merge offers fiat accounts in over forty currencies and stablecoin wallets for holding and converting between fiat and digital assets. Businesses can open multi‑currency accounts in 75+ countries without establishing a local entity. Local payment rails in more than 100 countries allow merchants to collect and disburse funds via bank transfers, instant payment schemes or card networks.

Intelligent Reconciliation and Treasury Tools

Merge automates reconciliation through virtual accounts, segregated sub‑accounts and maker‑checker permissions. This structure supports marketplaces and investment platforms that need to segregate client funds while maintaining compliance. API‑driven reporting gives finance teams real‑time insight into balances, settlement status and FX positions.

Compliance and Security

As a regulated platform, Merge safeguards client funds and adheres to strict compliance standards. Its stablecoin infrastructure is built on regulated partners and provides transparency over reserves. The platform’s API and webhook architecture integrates with existing back‑office systems, reducing manual intervention and streamlining operations.

By adopting Merge, businesses gain not only a payment orchestration platform but also a global treasury partner that combines stablecoin rails, multi‑currency accounts and intelligent reconciliation. This aligns with the narrative that payment acceptance is just the start; running an efficient payment operation across borders requires a higher‑order control layer.

Explore how Merge can simplify your global payment operations → Book a Demo

Disclaimer: This content is for informational purposes only and does not constitute financial, legal or regulatory advice. Businesses should seek independent professional guidance before implementing payment infrastructure or treasury solutions.

FAQ

What is the difference between payment orchestration and a payment gateway?

A payment gateway authorises and transmits individual transactions, acting as a secure bridge between the merchant, customer and acquiring bank. Payment orchestration platforms manage multiple gateways and providers, routing transactions intelligently, handling retries, reconciliation, reporting and compliance.

Do I need both a payment gateway and payment orchestration?

Yes. A gateway is required to authorise transactions, while orchestration adds optimisation and control across multiple providers. Together, they form a scalable, flexible payment stack.

Is payment orchestration only for enterprises?

No. While orchestration shines for high‑volume, multi‑market businesses, smaller merchants preparing for growth can benefit from a single integration that supports future expansion.

Can payment orchestration improve payment success rates?

Yes. By routing transactions through the provider most likely to approve them and automatically retrying failed payments, orchestration platforms can increase authorisation rates by double‑digit percentages.

What is a payment orchestration platform?

It is middleware that centralises payment gateways, processors, acquirers and other providers into a single API. It manages routing, retries, tokenisation, reconciliation, reporting and compliance.

Disclaimer: This content is intended for informational purposes only. It should not be considered financial, legal, or operational advice. Businesses should evaluate their own compliance, regulatory, and infrastructure requirements before implementing payment solutions.