Products

Multi-Currency Business Accounts

A multi-currency account lets your business hold, collect and send funds in multiple currencies from a single account, without converting every time.

Every time a payment is automatically converted into your bank account’s base currency, you lose margin to the bank's FX spread. A multi-currency bank account removes that step entirely. With Merge, your business holds funds in 60 currencies from a single account - collect in the sender's currency, pay out in the recipient's, and only convert when it makes commercial sense. Transparent fees, no embedded spreads.

Receive euros via SEPA Credit Transfer and SEPA Instant across the eurozone, with balances held in EUR. No automatic conversion on arrival - move funds when you choose, without FX spread before they land.

Receive sterling via Faster Payments and CHAPS, with balances held in GBP. No automatic conversion on arrival, no FX spread absorbed before the funds land in your account.

Hold US dollar balances and pay domestic and international counterparties in USD. A US dollar bank account accessible from anywhere your business operates, without forced FX conversion.

Receive, hold or send payments across more than 60 currencies. FX conversion only triggers where the send and receive currencies differ; conversion is a decision, not a default.

One account structure. Multiple currencies.

All accessible through a single API or dashboard.

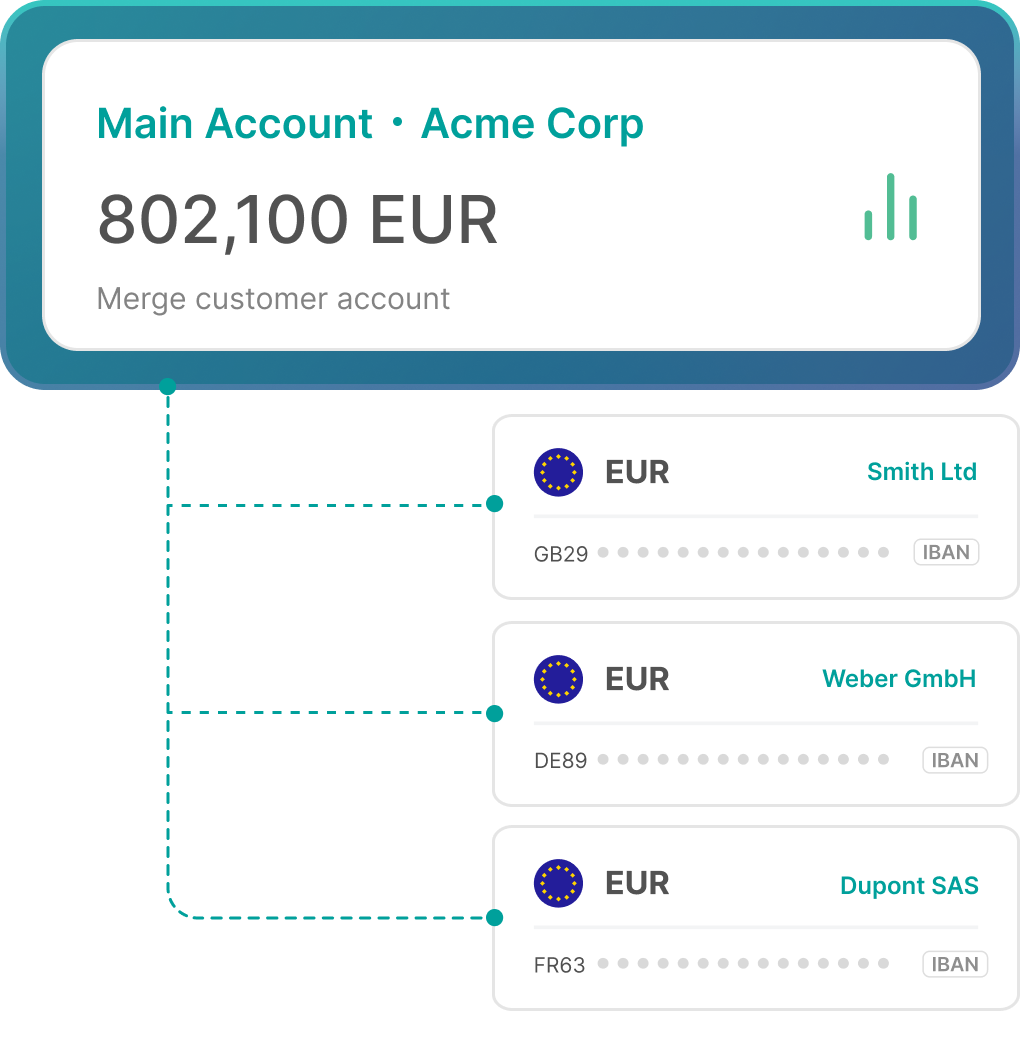

Open EUR accounts in your end customers' names - no new bank relationships required. Built for platforms collecting on behalf of users, marketplaces managing seller funds, and treasury teams running multi-entity structures across markets.

Most multi-currency virtual accounts are routing references, a number that directs inbound payments toward a pooled account. Merge's Named EUR IBANs are different. Each account is issued in the end customer's name and operates as a real and segregated account. Combining fiat collection, SEPA payments, and stablecoin rails in one API-first infrastructure.

Merge's multi-currency accounts are designed for fintechs, marketplaces, and corporate treasury teams where cross-border payments are core operations - not an occasional task. Named IBANs, seamless collection, and payments infrastructure that doesn't break when volume grows.

Building a multi-currency payments product from scratch means negotiating bank relationships in every currency corridor, maintaining a patchwork of banking APIs, and absorbing the operational burden of reconciliation across fragmented accounts, before you've written a single line of product code.

Merge's API gives you EUR, GBP and USD accounts, named IBANs for your end users, and local payment rails across 100+ countries, all through a single integration point.

Operating at the fiat-stablecoin intersection requires regulated fiat infrastructure that most payment providers are not built to support. Opening multi-currency accounts that connect to blockchain settlement rails typically means managing two separate vendor relationships, two compliance frameworks, and two reconciliation systems.

Merge provides multi-currency EUR, GBP and USD accounts alongside stablecoin on/off-ramp capability through the same regulated infrastructure and single API. Collect in fiat, settle in stablecoin, pay out globally, all within Merge's EMI and CASP regulatory framework.

Investment platforms handling client money across currencies face compounding compliance obligations: segregated client accounts per jurisdiction, FX transparency requirements, and reconciliation standards that leave no room for manual error. Standard banking infrastructure adds friction to every step.

Merge provides dedicated multi-currency account infrastructure with built-in compliance, full payment traceability, and real-time reconciliation. One integration handles client money collection, holding and distribution across EUR, GBP and USD.

When every seller gets paid in one currency, and your marketplace operates across borders, forced FX conversion erodes margin quietly. Sellers notice when their local currency payout loses value in transit. Your operations team notices when reconciliation takes two days instead of two minutes.

Collect from sellers in their local currency. Hold balances per seller in EUR, GBP or USD. Pay out in the currency that reaches them without loss baked into the transfer.

Talk to the Merge team and we'll configure the payment infrastructure that fits your use case.

The infrastructure question is not only what a platform can do, but whether the entity operating it can be trusted with the money. Here's why Merge belongs in both your technical stack and your compliance framework.

For fintechs that need both fiat rails and digital asset movement, Merge's stablecoin on/off ramp provides an adjacent capability within the same regulated infrastructure.

A multi-currency account is a single payment account that lets a business hold, receive and send money in multiple currencies without opening separate accounts per country. Balances are maintained in the original currency, in dedicated sub-accounts, until the business initiates a conversion or outbound payment.

Multi-currency accounting software refers to systems like Xero or QuickBooks that record, report and reconcile transactions denominated in multiple currencies. Merge is a payment infrastructure, not accounting software.

Inbound payments arrive via local rails, SEPA, Faster Payments, PIX, etc, and land in dedicated currency sub-accounts. Balances stay in the original currency until a disbursement instruction is issued. Outbound payments go in the recipient's currency; FX conversion only triggers where the send and hold currencies differ.

Contact Merge, describe your business requirements and currency corridors, then complete KYB onboarding through an API-driven process. EUR, GBP and USD accounts are available from day one after onboarding completes. There is no minimum transaction volume to access the core multi-currency account infrastructure. Onboarding timelines vary based on entity structure and jurisdiction complexity.

No. A virtual account is typically a routing reference that directs inbound payments to a pooled master account, identified by a unique reference number. Merge's Named EUR IBANs are real accounts issued in the end customer's name, they hold a live balance, support outbound payments, and appear in SEPA directories under the customer's identity. They are not aliases, and they are not pooled. The distinction matters for compliance, reconciliation accuracy, and the quality of the account experience visible to your end users.