Products

Stablecoin Payments Infrastructure

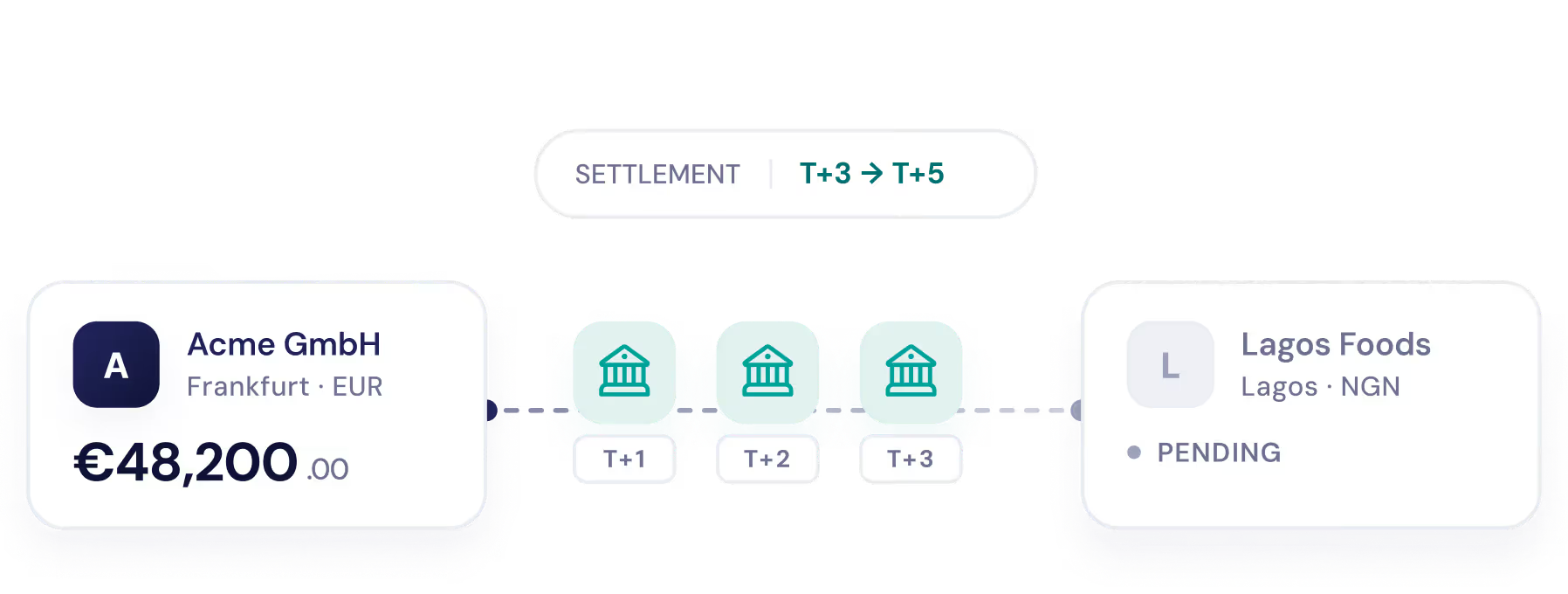

Stablecoin payments are cross-border transfers that settle in seconds using regulated, fiat-backed tokens, but typically require users to transact in stablecoins.

Merge combines stablecoin rails with local fiat payment networks, enabling seamless global transfers while senders and recipients continue to transact in fiat without changing how they operate.

Merge combines stablecoin rails with local fiat payment networks, enabling seamless global transfers while senders and recipients continue to transact in fiat without changing how they operate.