The role of virtual IBANs in modern banking

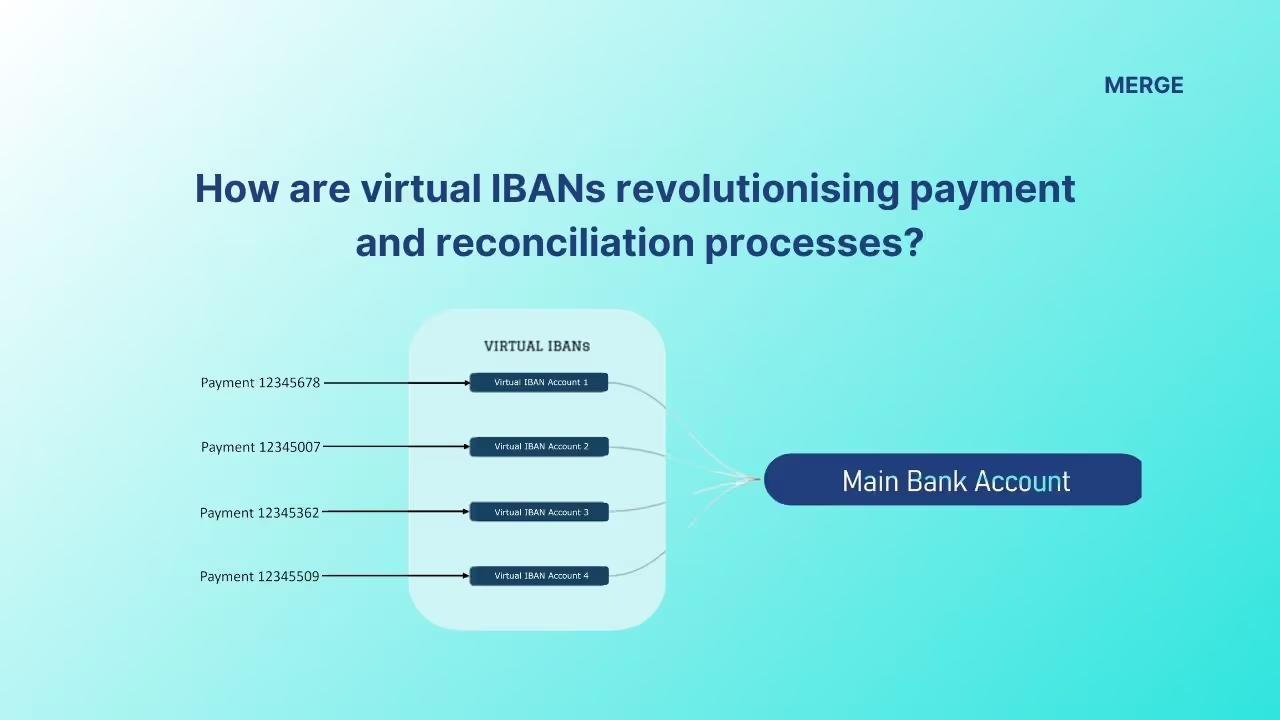

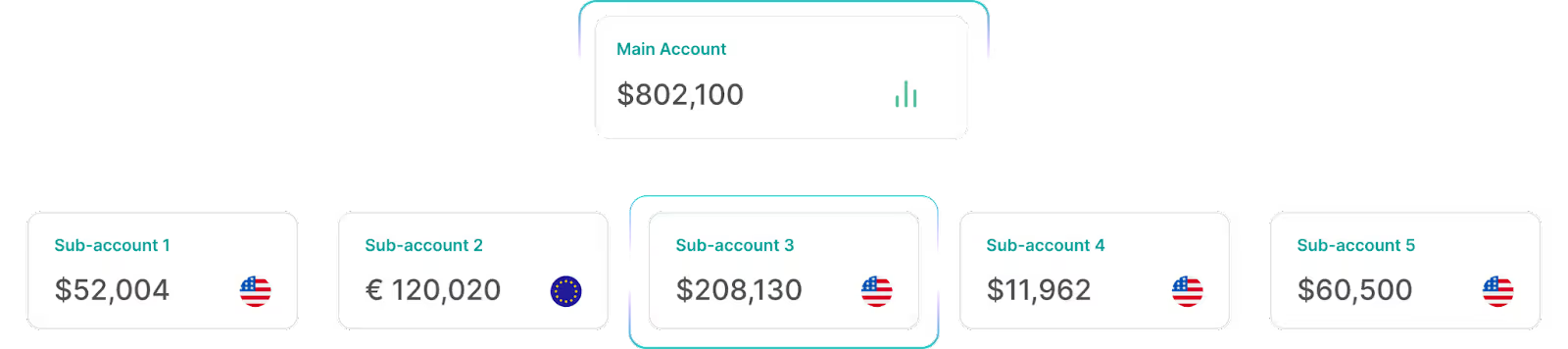

Virtual IBANs are digital account numbers that can be used to send and receive payments globally, without the need for a physical bank account. Functioning essentially as subledgers within a traditional bank's demand deposit account (DDA), virtual accounts divide and organise bank data. By assigning each transaction a unique identifier, or virtual account number, all payments are attributed to a discrete virtual account. This ensures that the total of all virtual accounts matches the physical accounts’ total. Essentially, these virtual accounts report the same information that a physical account does, only with enhanced precision and organisation.

How virtual IBANs contribute to making global payments seamless?

In an age of global commerce, businesses often find themselves dealing with multiple currencies, varied transaction fees, and the complexities of international payment regulations. For example, a UK-based e-commerce platform selling products to consumers across Europe would typically need to handle payments in GBP, EUR, USD, and more. Here, virtual IBANs play a crucial role. By assigning unique virtual IBANs to each customer or transaction type, the e-commerce platform can receive payments in multiple currencies directly to its primary bank account. This streamlines the reconciliation process since every payment can be automatically matched with its corresponding virtual IBAN, eliminating the hassle of manually sorting and matching transactions.

How virtual IBANs contribute to enhancing reconciliation processes through automation? Relevant use cases.

Consider a company that offers peer-to-peer payment solutions. With a growing user base spanning across different countries, reconciling payments becomes a considerable task. Virtual IBANs offer a solution. Each user is provided with a unique virtual IBAN, ensuring that when funds are transferred, they are directly linked to a specific user profile. This automated linkage drastically reduces errors.

Use case 1: Customer experience enhanced for remittance companies

Virtual IBANs enhance the customer experience for remittance companies by streamlining transactions. As explained above, each customer or transaction is assigned a unique virtual IBAN, which acts as a reference point within the banking infrastructure. When funds are transferred, this unique identifier ensures that transactions are processed quickly and accurately. Automated reconciliation, powered by these virtual IBANs, reduces errors by matching transactions to their respective identifiers. This minimises discrepancies and simplifies the backend processes. As a result, customers experience faster, more transparent, and error-free transactions.

Use case 2: Cashback processes

During a promotional event where companies offer cashback on transactions, using virtual IBANs can automate the cashback process. Instead of manually reviewing each transaction, the system can instantly verify transactions based on the virtual IBANs, ensuring timely and accurate cashbacks. This not only enhances user trust but also reduces the operational workload, allowing companies to focus on core business.

Use case 3: Buy Now Pay Later (BNPL)

In the BNPL model, online merchants offer their customers the option to pay in part payments. When a customer opts for this, the BNPL provider pays the full invoice to the merchant, then collects Instalments from the customer. Given the numerous transactions from various merchants and their respective clients, managing payouts and reconciliations becomes intricate. To streamline this, virtual IBANs are assigned for each deal. Upon a sale, the virtual IBAN registers the payment details, tracks instalments, and ensures timely collections. Once all instalments are paid, the deal is closed, and the virtual IBAN is reused. This centralised system aids in analytical accounting and gives a clear view of overall funds, benefiting financial planning and forecasting.

Use case 4: Liquidity management for crypto exchanges

Liquidity is crucial for a cryptocurrency exchange, influencing user experience, trading volumes, and platform reputation. Traders prefer exchanges with robust liquidity to execute large orders without major price slippage. Virtual IBANs offer a game-changing approach for these exchanges, streamlining liquidity management. With unique virtual IBANs for each user or transaction, payments can be tracked and matched swiftly, ensuring immediate fund availability. This not only accelerates transaction processing but also optimises cross-border transactions, leading to enhanced capital efficiency. As a result, exchanges can consistently maintain high liquidity levels, promoting a seamless trading environment.

How to set-up virtual IBANs efficiently for your business?

Banks and Fintechs provide a set of virtual IBANs for companies to allocate. Cost is an important consideration because this service attracts fees which can increase rapidly with large volumes of virtual IBANs. As a result companies often go for a capped number of virtual IBANs which they “recycle”, which means reassigning these virtual accounts once they are no longer required for their original purpose. Companies are best served when working with existing platforms that enable them to send, receive, and reconcile payments using a unified API and dashboard. To learn more, reach out to hello@merge.money.

Disclaimer: This content is intended for informational purposes only. It should not be considered financial, legal, or operational advice. Businesses should evaluate their own compliance, regulatory, and infrastructure requirements before implementing payment solutions.