API advancements in modern banking

In recent years, the integration of APIs within the global banking sector has transformed the financial services landscape. These technological conduits have unlocked various functionalities, from real-time payments, account aggregation, data retrieval, payment initiation to treasury management solutions.

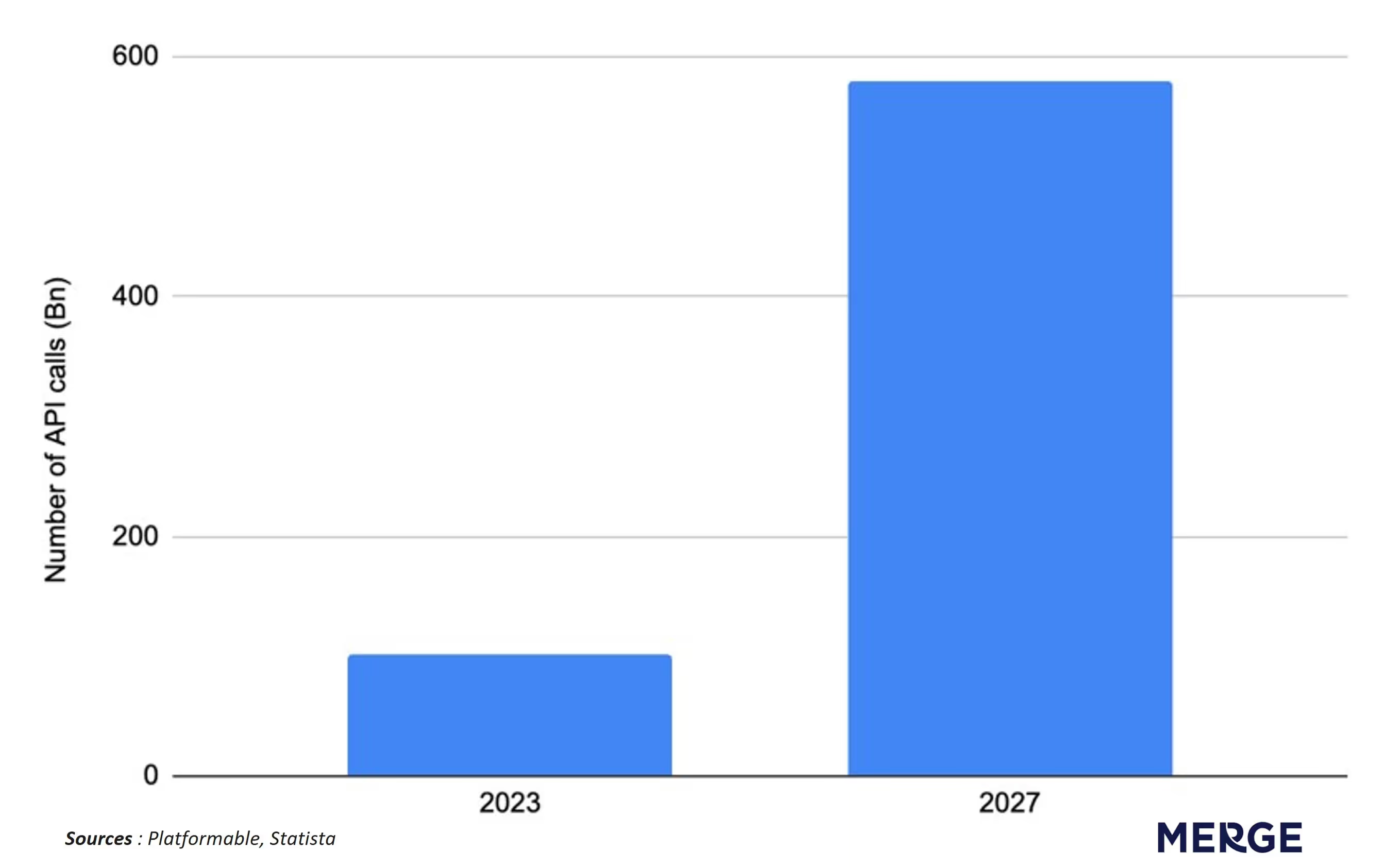

Furthermore, it's projected that open banking API calls will see an upward trend, increasing from 102 billion in 2023 to an anticipated 580 billion by 2027 worldwide.

Similarly, within that forecasted period, the estimated monetary value of open banking transactions is set to approach 330 billion U.S. dollars in 2027.

A breakdown by region and category

In Q2 2022, API offerings grew by 15% compared to the previous year. This growth was especially significant in regions like Latin America (56%), North America (35%), the UK (27%), and Asia Pacific (24%).

Also, in Q2 2022, research highlighted that worldwide, mandated APIs constituted an average of 62% of all banking APIs. Meanwhile, identity APIs accounted for 12%, credit services made up 6.5%, and the remainder comprised data services, trading, loyalty rewards, and other functionalities. This trend underscores banks' motivation to not only comply with regulatory mandates but also to diversify and enhance their API offerings in line with emerging market demands.

The significance of multi-currency management

In today's globalized business environment, managing transactions presents challenges like managing multiple currencies, understanding fluctuating exchange rates, and dealing with varied transaction fees. Yet, the true challenge for many companies, especially those juggling accounts in multiple banks, is obtaining a unified view of their financial standing. This is where banking APIs play a crucial role. By seamlessly integrating data from various bank accounts, APIs present a solution to the operational intricacies businesses face. These not only simplify tracking and transacting in different currencies but also provide real-time conversion rates, intricate risk management strategies, and sophisticated hedging options.

Case study: PSD2 and the need for customized cash management solutions

Introduced in January 2018, PSD2 European regulation led banks to develop APIs for PSPs, resulting in key standards like Germany's NextGenPSD2, the UK's Open Banking, and France's STET PSD2. These APIs primarily serve to access account data, initiate SEPA transfers, and confirm account funds. Despite their benefits, limitations like restricted SEPA transfer support and issues with authentication and reliability persist. Yet, driven by the potential of improved connectivity, banks are advancing towards crafting specialized cash management APIs.

Implications for businesses

As banking APIs become more prevalent, they are setting the stage for a new era in business operations. By consolidating information from multiple bank accounts into one dashboard, companies can make more informed financial decisions on the fly. Real-time data access ensures optimization of cash flows and facilitates proactive financial planning. Moreover, the enhanced capabilities these APIs bring—like streamlined payment processes and robust digital identity verification—minimise errors and improve operational efficiency. For businesses, this doesn't just mean easier management; it implies gaining a strategic edge in a fiercely competitive market.

Disclaimer: This content is intended for informational purposes only. It should not be considered financial, legal, or operational advice. Businesses should evaluate their own compliance, regulatory, and infrastructure requirements before implementing payment solutions.